Research

Working Papers

2023

-

Difference-in-differences with Economic Factors and the Case of Housing ReturnsSwiss Finance Institute Research Paper, 2023

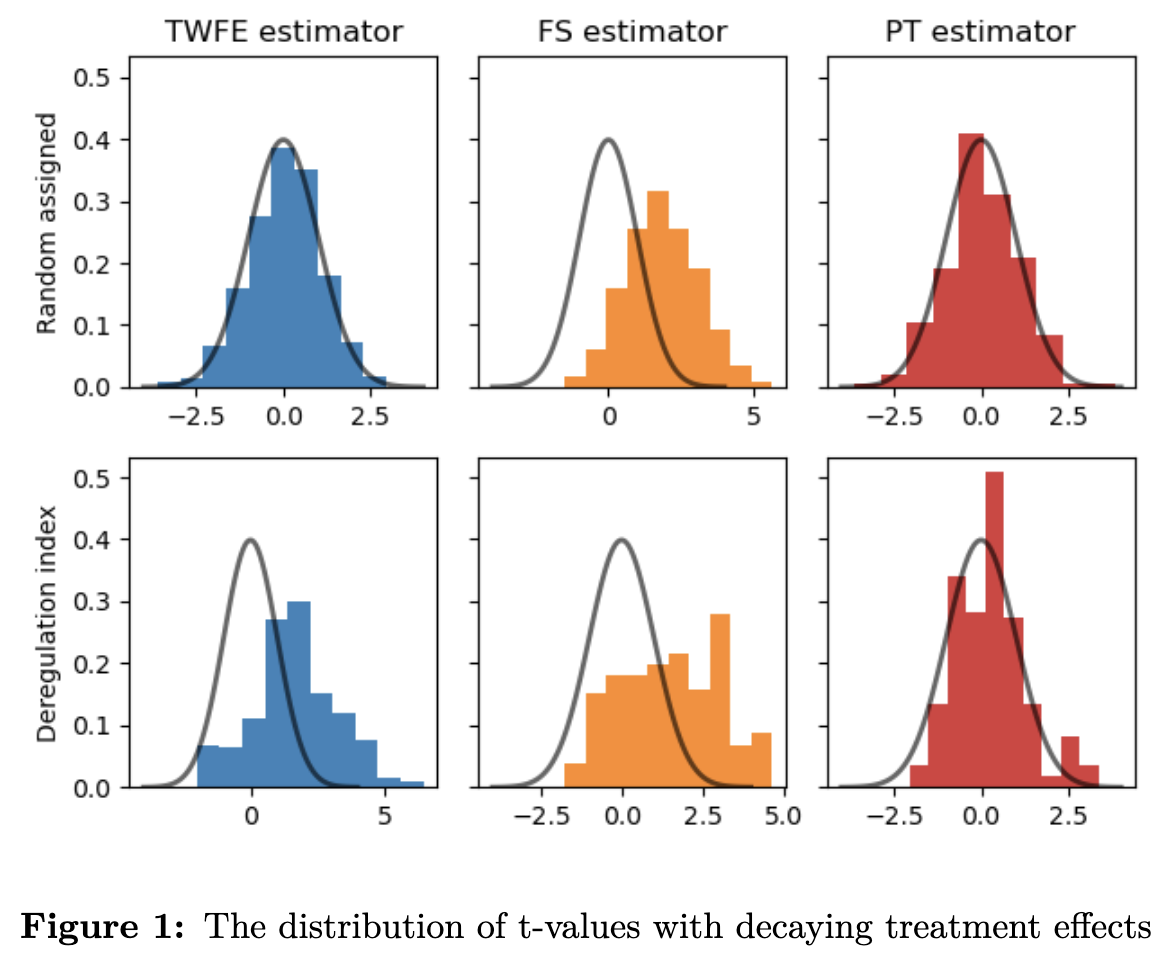

Difference-in-differences with Economic Factors and the Case of Housing ReturnsSwiss Finance Institute Research Paper, 2023This paper studies how to incorporate observable factors in difference-in-differences and document their empirical relevance. We show that even under random assignment directly adding factors with unit-specific loadings into the difference-in-differences estimation results in biased estimates. This bias, which we term the “bad time control problem” arises when the treatment effect covaries with the factor variation. Researchers often control for factor structures by using: (i) unit time trends, (ii) pre-treatment covariates interacted with a time trend and (iii) group-time dummies. We show that all these methods suffer from the bad time control problem and or omitted factor bias. We propose two solutions to the bad time control problem. To evaluate the relevance of the factor structure we study US housing returns. Adding macroeconomic factors shows that factors have additional explanatory power and estimated factor loadings differ systematically across geographic areas. This results in substantially altered treatment effects.

2018

-

The Sovereign Debt Crisis: Flights or Freezes?Swiss Finance Institute Research Paper, 2018

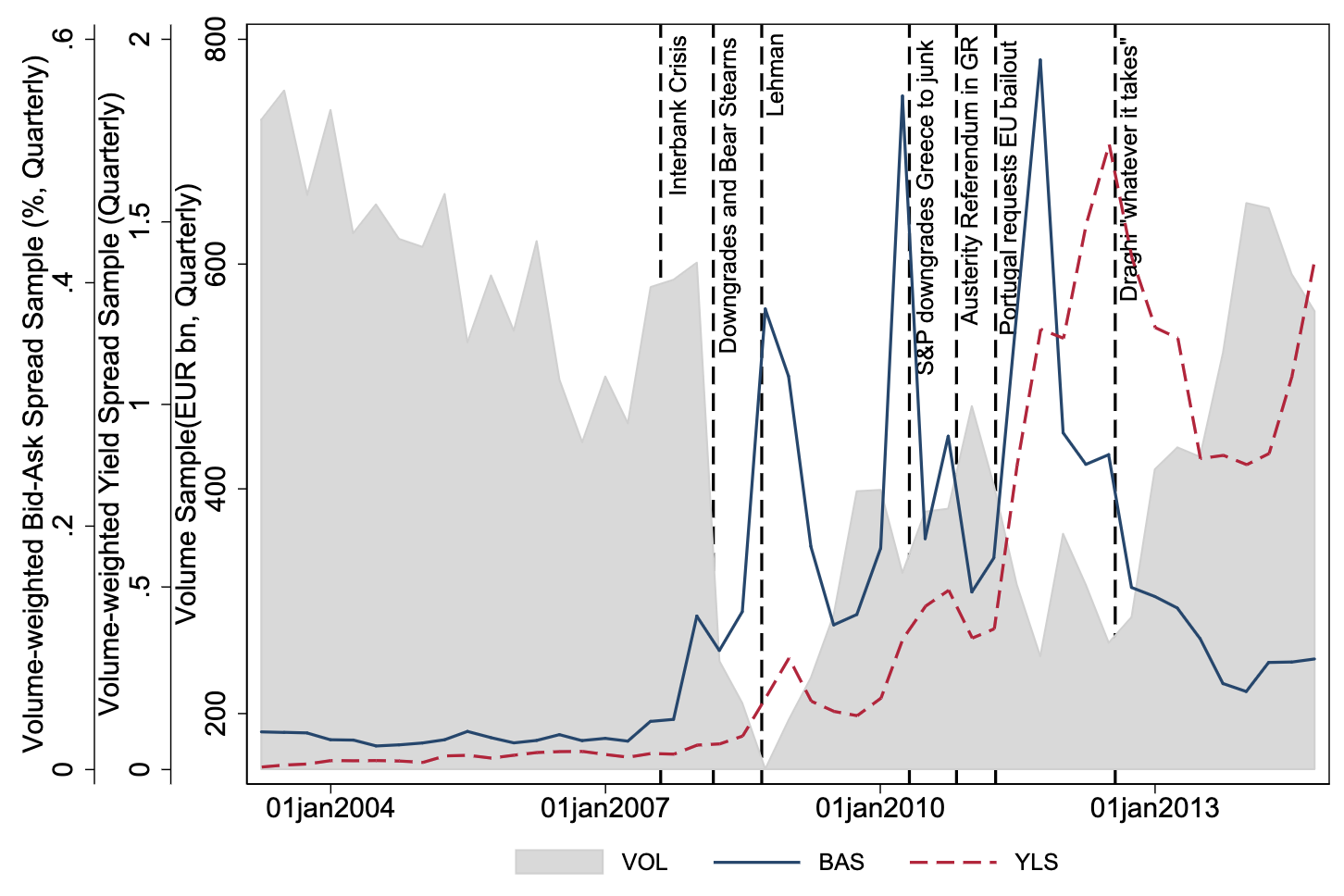

The Sovereign Debt Crisis: Flights or Freezes?Swiss Finance Institute Research Paper, 2018Multiple asset pricing theories predict that large price changes should be associated with abnormal trading volume, inducing investor rebalancing and possibly leading to flights. In contrast, consistent with market microstructure theories, this paper documents freezes, a reduction in trading volume (approximately 30% relative to the previous trading week) during market stress episodes in the European sovereign bond market. We trace the market freezes to increasing transaction costs driven by reduced risk bearing capacity of market makers.

Published Papers

2015

2014

-

Money and liquidity in financial marketsJournal of Financial Economics, 2014

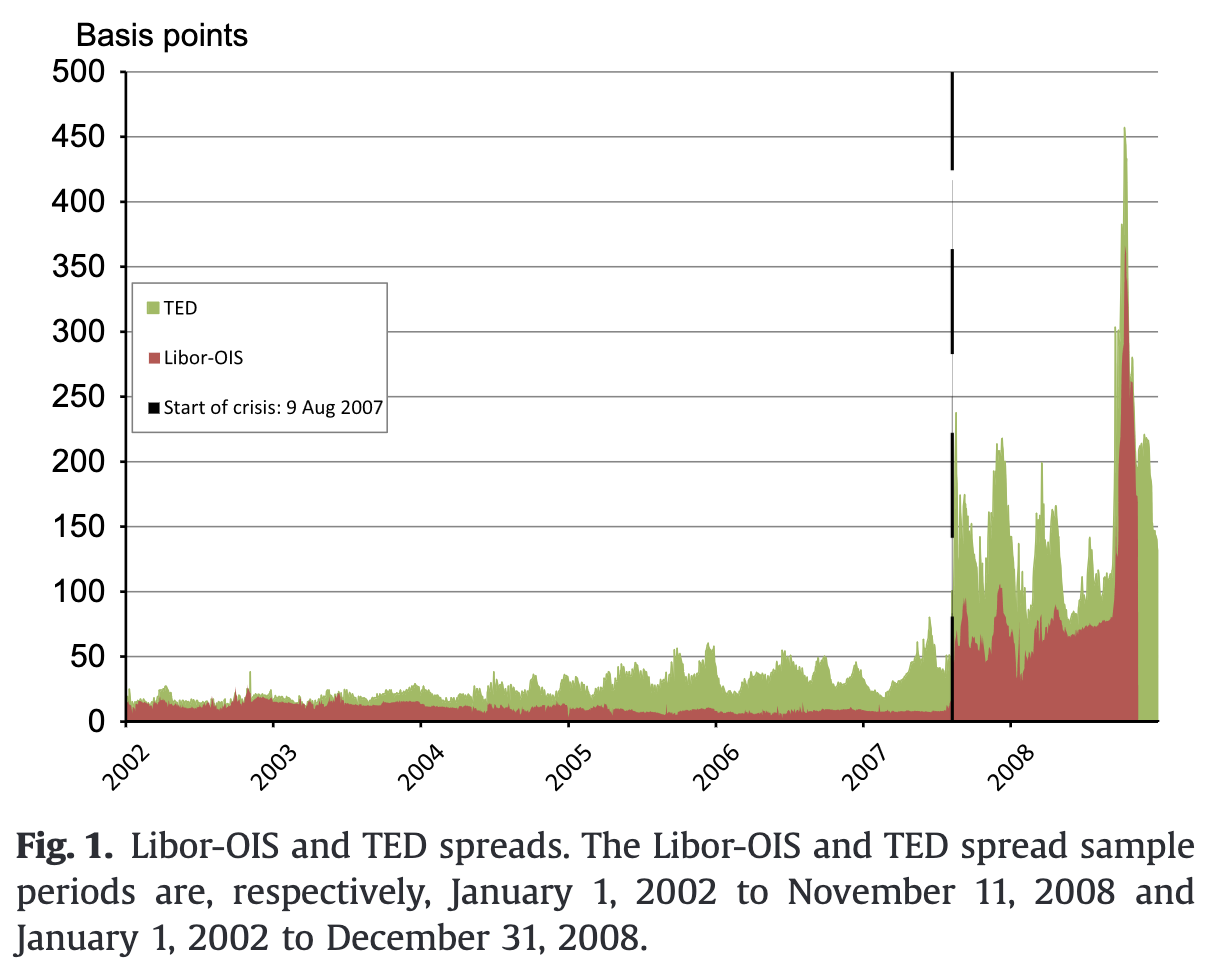

Money and liquidity in financial marketsJournal of Financial Economics, 2014We argue that there is a connection between the interbank market for liquidity and the broader financial markets, which has its basis in demand for liquidity by banks. Tightness in the market for liquidity leads banks to engage in what we term “liquidity pull-back,” which involves selling financial assets either by banks directly or by levered investors. Empirical tests on the stock market are supportive. Tighter interbank markets are associated with relatively more volume in more liquid stocks; selling pressure, especially in more liquid stocks; and transitory negative returns. We control for market-wide uncertainty and in the process also contribute to the literature on portfolio rebalancing. Our general point is that money matters in financial markets.

2013

2009

-

Does investor recognition predict returns?Journal of Financial Economics, 2009

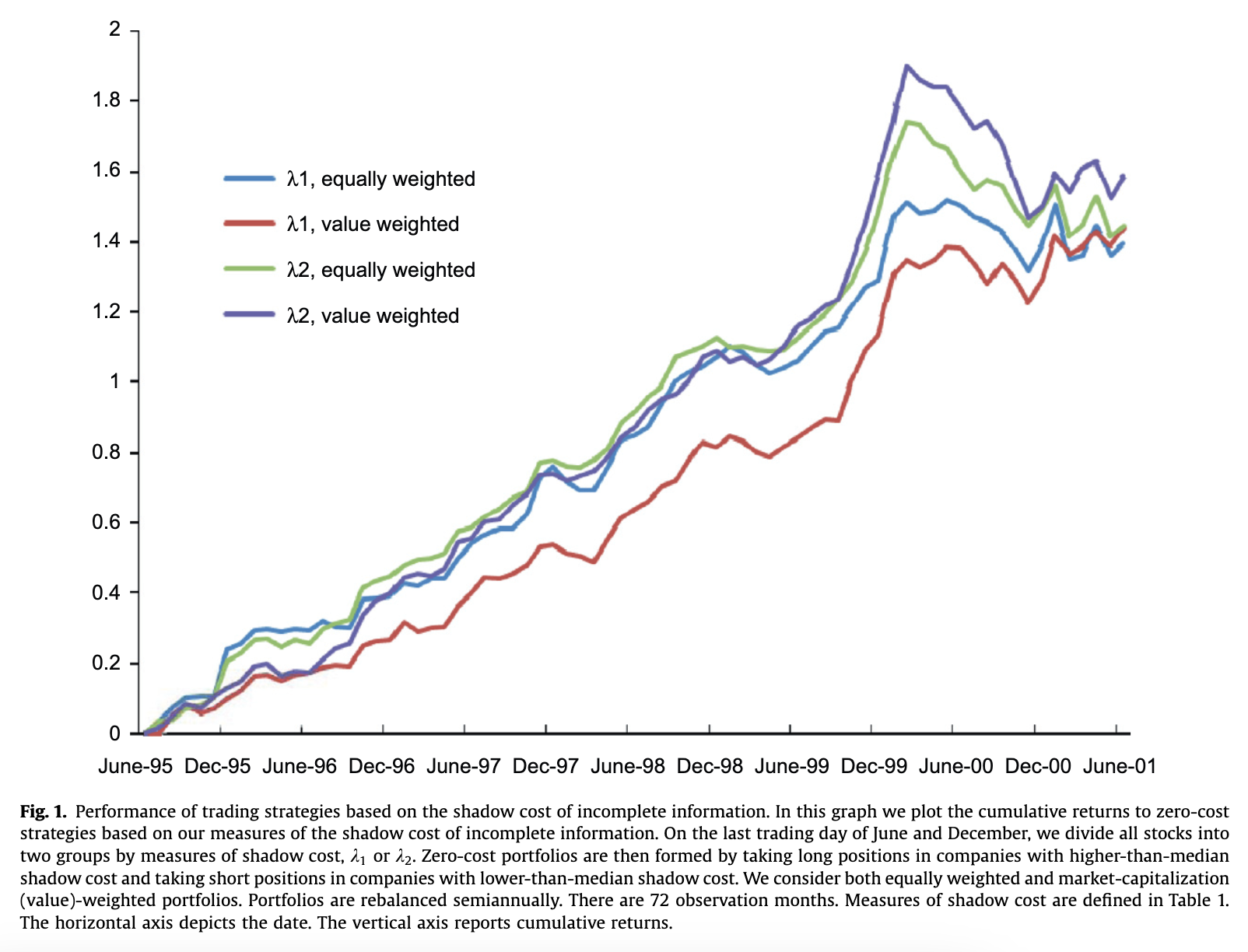

Does investor recognition predict returns?Journal of Financial Economics, 2009Merton [1987. A simple model of capital market equilibrium with incomplete information. Journal of Finance 42, 483–510] shows that stocks about which not all investors are informed should yield a return premium. This premium depends on the shadow cost of incomplete information which in turn depends on the shareholder base, relative market size, and idiosyncratic risk. Utilizing a comprehensive database of Swedish shareholdings, we demonstrate that stock returns are positively related to the shadow cost. We also find that the shareholder base is negatively related to returns when controlling for size and idiosyncratic risk. Zero-cost portfolios based on the shadow cost/shareholder base yield substantial trading profits that are never positively correlated with the market and are only modestly explained by the four-factor model.

2006

- Disclosure, investment and regulationJournal of Financial Intermediation, 2006

This paper provides a framework to analyze voluntary and mandatory disclosure. Since improved disclosure reduces the entrepreneur’s ability to extract private benefits, it secures funding for new investments, but also provides existing claimholders with a windfall gain. As a result, the entrepreneur may choose to forgo investment in favor of extracting more private benefits. A mandatory disclosure standard reduces inefficient extraction and increases investment efficiency. Although the optimal standard is higher than the entrepreneur’s optimal choice, it can be less than complete in order not to deter investment. The model also shows that better legal shareholder protection goes together with higher disclosure standards and that harmonization of disclosure standards may be detrimental.